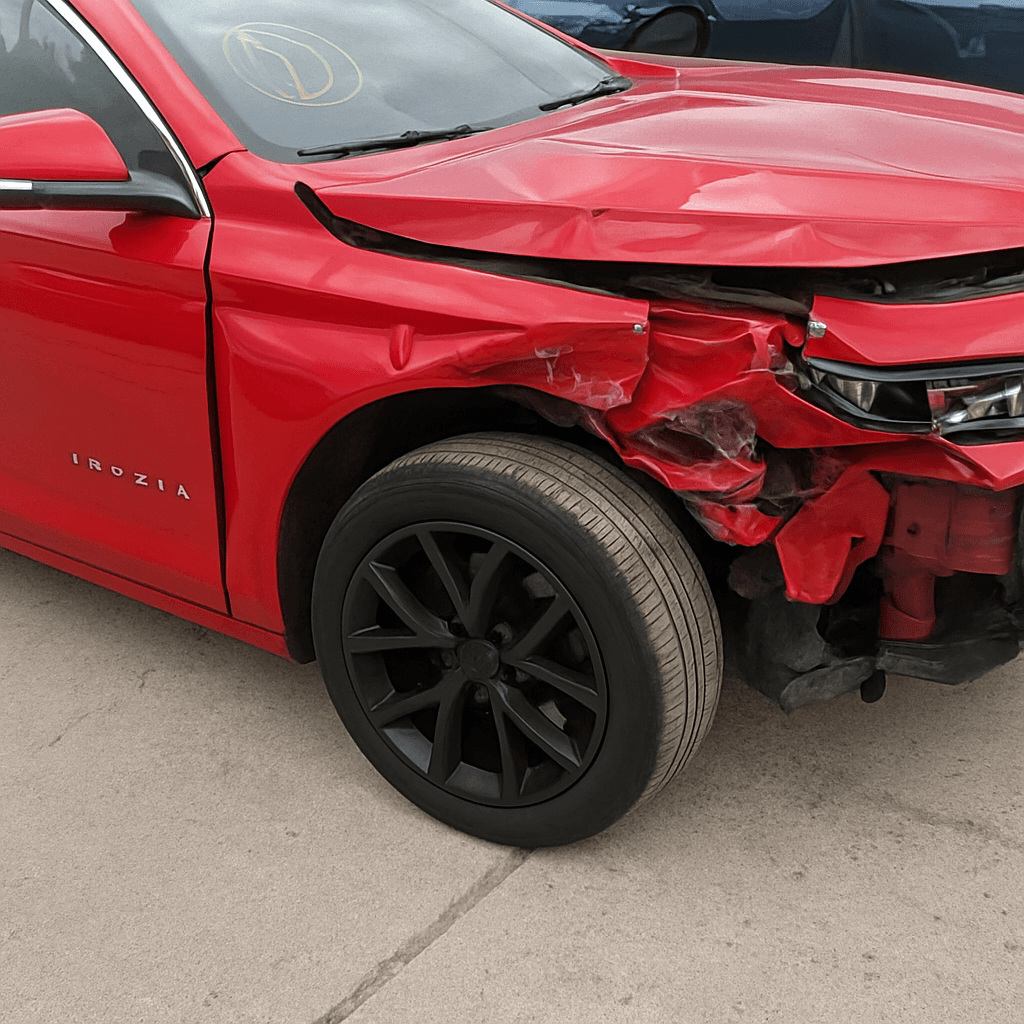

When you cause an accident in a rental car, the violation follows your personal driving record — not the rental agreement. The points, rate increase, and potential suspension apply exactly as if you were driving your own vehicle.

Your Personal Driving Record Takes the Hit, Not the Rental Agreement

An at-fault accident in a rental car appears on your personal driving record within 30-60 days of the accident report filing. The state DMV assigns points based on the violation severity — typically 2-4 points for an at-fault accident with property damage, and 4-6 points if the accident involved bodily injury. The rental agreement does not shield your record.

Your personal auto insurance policy covers rental vehicles under the liability and collision sections in most states, which means your carrier processes the claim, assigns fault, and applies the surcharge to your renewal premium. If you declined personal coverage and used a credit card's rental protection or the rental company's damage waiver, the accident still generates a police or incident report that flows to the DMV. The report triggers point assignment regardless of which insurance paid the claim.

Drivers often assume the rental company's involvement somehow isolates the violation. It does not. The DMV receives accident reports from law enforcement and processes them against the driver's license number on the report — which is yours, not the rental company's. Point assignment follows the same schedule as any other at-fault accident, and the points remain on your record for the state's standard lookback period, typically 3-5 years.

How Carriers Apply Rate Increases After a Rental Car Accident

Your insurance carrier applies a surcharge at renewal after an at-fault accident in a rental vehicle, typically 20-40% for a first accident and 50-80% for a second accident within three years. The surcharge duration runs 3-5 years depending on the carrier's rating schedule and state regulations. The fact that you were driving a rental does not reduce the surcharge.

If your personal policy covered the rental and you filed a claim, the carrier codes the loss as an at-fault collision. That coding triggers the surcharge automatically at the next renewal. If you used alternate coverage — credit card protection, the rental company's damage waiver, or paid out of pocket — the carrier still learns of the accident when they pull your motor vehicle report (MVR) at renewal or when the state transmits the violation to the carrier directly in real-time reporting states.

Some drivers attempt to avoid filing a claim by using the rental company's insurance or paying repair costs directly, hoping to keep the accident off their personal carrier's radar. This strategy fails because the DMV point assignment appears on your MVR regardless of who paid for the damage. Carriers review MVRs at every renewal, and the accident surfaces then. The surcharge applies at the first renewal after the carrier discovers the violation, even if that discovery happens a year after the accident date.

Compare rates from carriers that work with drivers who have points

Standard carriers surcharge heavily after violations. These specialists price your specific record differently.

Get Your Free Quote✓ Violation Specialists✓ No Obligation✓ Licensed Carriers✓ All Point Levels

When a Rental Accident Pushes You Over the Suspension Threshold

If the rental car accident adds points that push your total over your state's suspension threshold — typically 8-12 points in a 12-24 month rolling window — the DMV initiates a license suspension. The suspension process begins 30-45 days after the accident report posts to your record, giving you a narrow window to request a hearing or enroll in a state-approved defensive driving course if your state allows point reduction before suspension takes effect.

States that use conviction-count systems rather than numeric points apply the same logic. A rental car accident counts as one conviction. If that conviction is your second or third within the lookback period, and your state suspends licenses after two or three convictions, the suspension applies. The vehicle type does not matter — the DMV counts the violation against your personal driving privilege.

Once suspended, you lose the ability to drive legally, and reinstatement requires paying fees, completing any court-ordered programs, and filing proof of insurance with the DMV. Some states require SR-22 or FR-44 filing after a points-triggered suspension, which adds $15-50 in annual filing fees and often forces you into the non-standard insurance market where monthly premiums run $150-$300 for minimum liability coverage. Drivers who ignore the suspension notice and continue driving face additional charges for driving under suspension, which typically adds 6-8 more points and extends the suspension period by 6-12 months.

What Happens If You Were Driving the Rental for Business

An at-fault accident in a rental car during a business trip still assigns points to your personal driving record. The DMV does not distinguish between personal and business use when processing accident reports. The driver's license on the police report receives the points, and your personal insurance carrier applies the surcharge at renewal.

If your employer's commercial auto policy or a corporate rental agreement covered the vehicle, that coverage pays the property damage and injury claims, but the violation follows your license. Some drivers assume a corporate policy insulates their personal record — it does not. The accident report identifies you as the at-fault driver, and the state processes that report against your personal DMV file.

Your personal carrier may subrogate against the business policy to recover claim payments, but the MVR coding and point assignment remain unchanged. The surcharge applies at your next personal policy renewal. If you carry a personal policy and the employer's policy also applies, coordination-of-benefits rules determine which carrier pays first, but both carriers treat the accident as a chargeable loss, and both may apply surcharges if their underwriting guidelines include business-use accidents.

How to Minimize Rate Impact After the Accident Posts

The most effective step is completing a state-approved defensive driving course within 60-90 days of the accident if your state allows point reduction for voluntary course completion. Courses cost $25-$75 and remove 2-4 points in states that offer point reduction, which can prevent a suspension if you were near the threshold. The course completion does not erase the accident from your MVR, but it reduces the active point total the DMV uses to calculate suspension eligibility.

Request a rate review with your current carrier after completing the course. Some carriers re-rate your policy mid-term if you provide a course completion certificate, which reduces your premium before the next renewal. Other carriers apply the discount only at renewal. If your carrier refuses to adjust the rate or non-renews your policy after the accident, request quotes from at least three competitors. Carriers weight accidents differently — one carrier may surcharge 40% while another surcharges 25% for the same violation. Rate spreads widen after an accident, so the lowest-cost carrier for a clean record may not be the lowest-cost option once points appear.

If the accident pushed you into the non-standard market, expect monthly premiums of $150-$300 for state minimum liability coverage. Non-standard carriers accept drivers with multiple points but charge higher base rates and apply stricter underwriting rules. After 3-5 years without additional violations, you can re-enter the standard market, and your rate drops 30-50% compared to the non-standard premium. Avoid filing claims during the surcharge period unless the damage exceeds 2-3 times your annual premium — each additional claim extends the surcharge period and increases the risk of non-renewal.

Why the Rental Company's Coverage Does Not Protect Your Record

The rental company's liability insurance or damage waiver covers the vehicle's repair costs and third-party injury claims, but it does not prevent the DMV from assigning points to your license. Insurance and DMV point systems operate independently. Paying for damage through the rental company's coverage instead of filing a claim on your personal policy eliminates the insurance claim but does not erase the accident report.

Law enforcement files accident reports with the state DMV after any collision involving injury, property damage over a threshold amount (typically $500-$1,500 depending on the state), or a citation issued at the scene. The DMV processes that report and assigns points based on the violation type and fault determination. The report identifies you as the driver, and the points post to your license regardless of which insurance paid for repairs.

Some drivers pay the rental company's repair invoice out of pocket to avoid involving any insurance. This approach prevents an insurance claim from appearing on your claims history report (CLUE), but it does not stop the DMV from processing the accident report. The points still appear, and your carrier still discovers the accident when they pull your MVR at renewal. The only scenario where an accident might not generate a DMV report is a minor parking lot collision with no police response, no injuries, and damage under the state's reporting threshold — but if the rental company files an incident report or the other party reports the accident, the DMV receives notification and processes the violation.