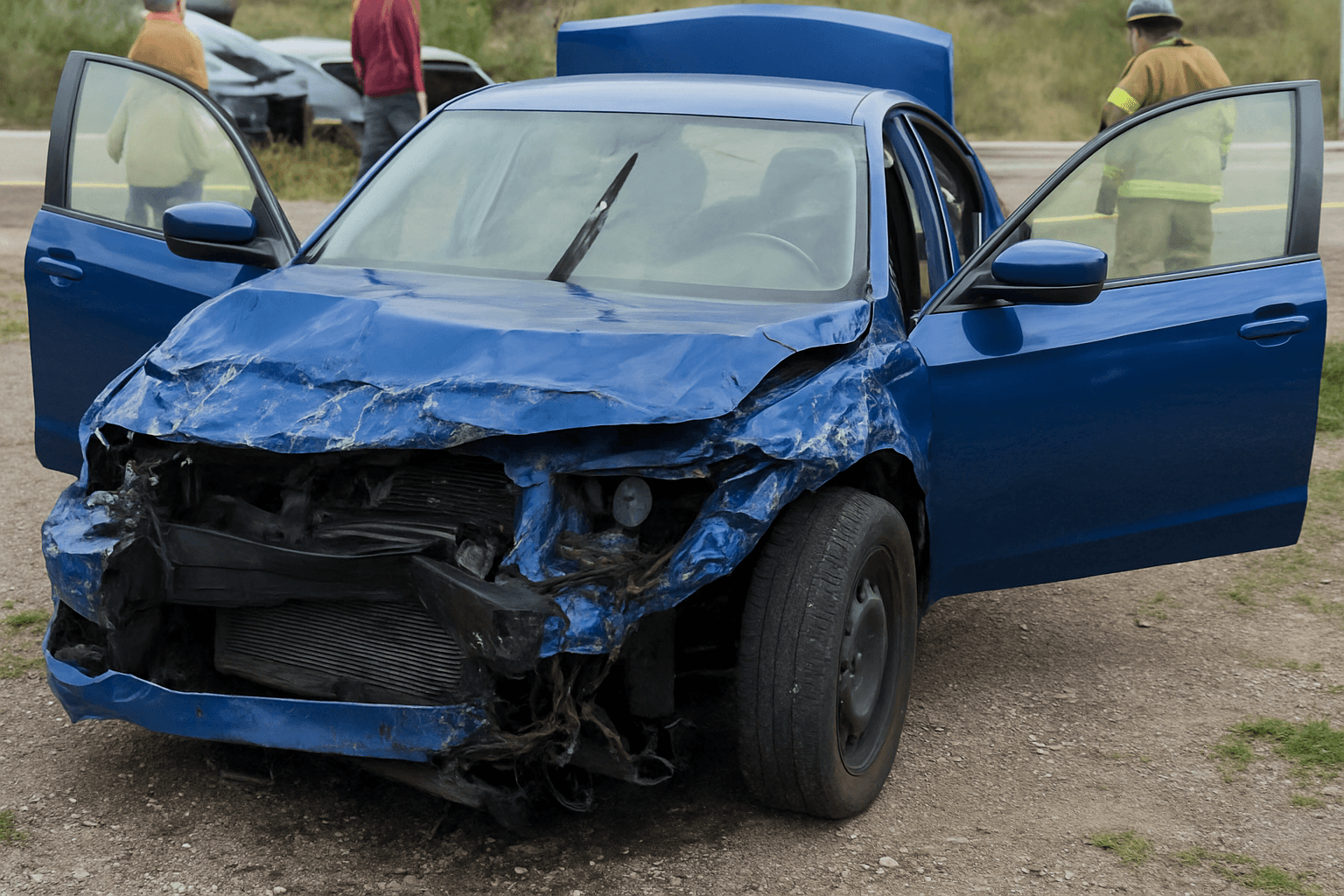

An at-fault accident with bodily injury triggers both a DMV point assignment and a multi-year carrier surcharge—and the two systems run on different clocks.

Why bodily injury accidents stack points and surcharges differently

An at-fault accident with bodily injury typically adds 3-4 points to your DMV record in most states and triggers a carrier surcharge that lasts 3-5 years. The point assignment comes from the state; the surcharge comes from your insurer's underwriting rules. These two consequences operate independently.

Points usually drop off your DMV record after 2-3 years, depending on state law. Carrier surcharges persist based on the carrier's claims lookback period—most major carriers review your last 3-5 years of claims history at each renewal. A bodily injury claim with a payout over $2,500 stays visible in industry loss databases for 5-7 years, which means even after your state removes the points, the accident remains part of your insurance pricing profile.

This is why your rate doesn't automatically drop when points expire. The carrier isn't tracking your DMV points—they're tracking the claim. You need to understand both clocks if you want to predict when your premium recovers.

How carriers price bodily injury accidents at renewal

Carriers assign surcharge percentages based on claim severity, not point values. A bodily injury accident with a $5,000 medical payout typically triggers a 30-50% rate increase at your next renewal. A $25,000 payout can double your premium or push you into non-standard coverage.

The surcharge applies for the carrier's full lookback window, which runs 3-5 years from the accident date under current underwriting rules. State Farm and Allstate typically use 3-year lookback periods; Progressive and GEICO use 5-year windows. If you stay with the same carrier, the surcharge diminishes gradually—many carriers reduce it by 10-20% annually after year two if no new claims appear.

Switching carriers won't erase the accident. Every insurer pulls your CLUE report during underwriting, which lists all claims filed in the last 7 years. A carrier offering a quote after a bodily injury accident is pricing that risk into the premium from day one.

Compare rates from carriers that work with drivers who have points

Standard carriers surcharge heavily after violations. These specialists price your specific record differently.

Get Your Free Quote✓ Violation Specialists✓ No Obligation✓ Licensed Carriers✓ All Point Levels

When bodily injury accidents trigger license suspension

Most states don't suspend your license for a first at-fault accident unless you accumulate enough total points to cross the suspension threshold within a rolling window. A single accident with 3-4 points won't suspend you in most states, but if you already have 4-6 points from speeding tickets, the accident pushes you over.

Suspension thresholds vary widely. Ohio suspends at 12 points in 2 years. California suspends at 4 points in 12 months. Virginia uses a demerit system where 18 points in 12 months triggers suspension. If your accident crosses the threshold, expect a DMV suspension notice within 30-60 days and a requirement to file SR-22 upon reinstatement.

Some states also suspend your license if you cause an accident without insurance or fail to pay a judgment from a bodily injury lawsuit. These are financial-responsibility suspensions, not point-based suspensions, and they require SR-22 filing for 3-5 years depending on the state.

How long the rate increase lasts after bodily injury

Your premium stays elevated until the accident falls outside your carrier's lookback window. For most drivers, that means 3-5 years of surcharges starting from the accident date. The surcharge doesn't wait for your renewal—it applies the moment your policy renews after the claim closes.

If you switch carriers during the surcharge period, the new carrier prices the accident into your quote. You might save money by shopping, but you won't escape the accident surcharge entirely. Non-standard carriers like The General or Safe Auto quote drivers with recent bodily injury claims, but their base rates are higher and they apply their own accident surcharges on top.

After 5 years, most accidents stop affecting your rate. Preferred carriers like State Farm and Allstate treat you as a clean-risk driver again once the claim ages past their lookback window. If you've maintained continuous coverage and added no new violations, you'll qualify for standard pricing.

What defensive driving courses do for bodily injury points

Defensive driving courses remove 2-3 points from your DMV record in most states, but they don't erase the accident claim from your CLUE report. If your state allows point reduction through a course, completing one within 90 days of the accident keeps you further from suspension and may prevent additional surcharges if you're close to a multi-violation tier.

The course affects your DMV record, not your insurance directly. You need to request a rate review after completing the course—most carriers won't automatically adjust your premium until the next renewal. Some carriers offer a defensive driving discount separate from the accident surcharge, which can offset 5-10% of the increase.

Not every state allows point reduction for at-fault accidents. California, for example, doesn't remove points for traffic school if the violation involved an accident. Check your state DMV's eligibility rules before enrolling in a course.

How to shop for coverage after a bodily injury accident

Get quotes from at least three carriers within 30 days of your renewal notice. Preferred carriers like Erie, Auto-Owners, and American Family sometimes offer better post-accident pricing than the national brands, especially if you've been with your current carrier for less than 3 years. Regional carriers weigh claim history differently.

Non-standard carriers like Bristol West, Dairyland, and National General specialize in high-risk drivers and will quote you immediately after a bodily injury claim. Their base rates run 40-80% higher than preferred carriers, but if your current carrier is threatening non-renewal, a non-standard policy keeps you legal and insured while your record clears.

Don't cancel your current policy before the new one binds. A lapse in coverage after a bodily injury accident raises your rates further and can trigger an SR-22 requirement in some states. Bind the new policy effective the same day your old policy ends.

When SR-22 filing enters the picture

SR-22 filing becomes mandatory if your bodily injury accident triggers a license suspension or if you were uninsured at the time of the accident. Most states require 3 years of continuous SR-22 filing after reinstatement. The filing itself costs $15-50, but SR-22 drivers pay 50-100% more for coverage because only non-standard carriers write SR-22 policies.

If your accident didn't trigger suspension and you were insured, you don't need SR-22. Points alone don't require filing—suspension does. If you're unsure whether your state requires SR-22 after your accident, check your reinstatement notice from the DMV or call your state's driver services line.

SR-22 surcharges stack on top of accident surcharges. A bodily injury accident with SR-22 filing typically results in premiums 2-3 times your pre-accident rate. The SR-22 requirement expires after 3 years of continuous filing, but the accident surcharge persists until it falls outside the carrier's lookback window.